April 2026 | ![]() 11 min read | Download PDF

11 min read | Download PDF

Summary

Lately, private credit has been in the headlines more than usual. Against this backdrop, our private credit portfolios have continued to remain stable due to what we regard as our sensibly conservative positioning in the asset class.

Disciplined underwriting, focusing on borrowers with robust free cash flow, stringent covenant protections, and consistent use of first lien senior secured structures are hallmarks of our approach.

Through bespoke investment mandates in our stand alone, fund of one arrangements with specialist private credit managers, we retain control over key underwriting standards. These mandates require stringent covenants and conservative loan terms, including low leverage and strong interest coverage ratios, giving us confidence in borrowers’ ability to service their debt across a range of conditions.

Importantly, we also maintain full transparency over the underlying loans originated by our appointed managers. This level of visibility is markedly different from the experience of investors accessing private credit through pooled retail vehicles, where insight into individual exposures is often limited.

We have deliberately avoided areas of the market now under stress including semi liquid business development companies (BDCs), highly leveraged software borrowers, and opaque asset backed finance structures while maintaining broad industry diversification along with modest subsector exposures.

This has enabled us to deliver risk adjusted returns above traditional fixed income and positions us well to take advantage of emerging opportunities as more capital constrained lenders retreat.

We recognise that recent developments in private credit have understandably unsettled some investors. However, we believe these events should be viewed in proper context. In our assessment, the challenges have been idiosyncratic rather than systemic, stemming from liquidity mismatches in semi liquid or retail oriented vehicles, governance weaknesses, and structural design flaws. As we see it, they are not indicative of widespread credit deterioration.

We believe private credit programs anchored to manager and sector diversification, institutional grade governance, and a disciplined approach to risk will continue to be valuable parts of well-diversified investment portfolios.

The sections that follow address each of the recent areas of market attention and provide a clear window into our investment philosophy and approach to the asset class.

Tensions stemming from liquidity expectations in an illiquid asset class

Over the past year, business development companies (BDCs) have become a problem child in private credit. This, however, has not derived from stresses in underlying loan performance but rather from a structural mismatch between illiquid assets and investors expecting liquidity.

By design, BDCs were intended to democratise access to private credit: regulated US vehicles originating loans, mainly senior secured debt, to small and mid sized companies.

As appetite for private credit grew rapidly from around 2020 through 2024, large asset managers, including Blackstone, and Blue Owl, amongst others, raised tens of billions of dollars through BDCs, which are non traded or semi liquid structures.1 Nevertheless, BDCs promised regular income and limited quarterly redemption windows. The structures worked well so long as flows were positive and returns stayed buoyant.

When sentiment soured from around late 2025, retail investor liquidity requests swelled, something these fund vehicles were not built to deliver. These structures were designed for modest scale redemptions not something of the magnitude of redemptions that occurred.

The most visible pressure emerged at Blue Owl, whose non exchange traded Blue Owl Capital Corporation II (OBDC II) fund faced redemption requests more than twice its roughly 5% of net asset value quarterly cap.2 In early 2026, Blue Owl halted redemptions and shifted the fund into an orderly liquidation process, effectively converting it from a semi liquid income vehicle into a run off pool.3

An aborted consolidation

The events followed Blue Owl’s aborted 2025 merger attempt to combine its OBDC II fund with its publicly listed OBDC fund.4 That deal, pitched as a liquidity solution for investors, came undone amid backlash over proposed valuation discounts. The failed integration left OBDC II’s investors locked in precisely the structure they had hoped to escape.

The episode has become a kind of shorthand for a broader liquidity mismatch problem across the sector deriving from structures with liquidity expectations, which were going to be challenging owing to the illiquidity of the asset class’s underlying investments.

The timing proved critical. As Blue Owl shut its gates, funds from the likes of BlackRock, Cliffwater, and Morgan Stanley hit structural redemption limits too, each only able to honour a fraction of investor withdrawal requests.5

The cascade of soft freezes has rattled investors, even though most underlying loans remained performing and default rates stayed modest.

The same period saw a broader stall in consolidation efforts across large private credit platforms. Several managers that had marketed retail accessible BDCs explored mergers or rebrandings to preserve scale and liquidity, yet most deals were shelved. Market participants pointed to valuation gaps, regulatory uncertainty, and diverging investor bases as reasons these proposals never materialised.

By early 2026, the cumulative effect was visible in fund flows and unit prices. Many non exchange traded BDCs were marked down to the high 70 cents on the dollar range, reflecting investor scepticism about both valuations and governance.6

Key takeaways

We have been offered the opportunity of participating in BDCs on numerous occasions and have turned them down each time deeming BDCs to be inappropriate structures for private credit investing. BDCs blur the line between institutional direct lending and mass market distribution, a tension that has led to recent wrinkles.

From our observations as well as direct experience, private credit remains sound at the portfolio level, but the kind of ‘retail wrappers’ associated with BDCs demand better governance, disciplined liquidity design, and clear communication. To us, the BDC volatility of 2025/26 ought to hasten the industry’s maturation into a phase where structure and transparency matter as much as returns.

Frauds: small in numbers, large in controversy

Several fraud events in the second half of 2025 through early 2026 have also contributed to reputational damage. While these issues were confined to specific areas, particularly asset backed finance and lending to large companies, they triggered a reassessment of governance and risk discipline across the asset class.

High profile cases, including those tied to First Brands,7 Tricolor,8 Brahmbhatt Capital,9 and MFS10 appear to stem not from traditional core mid market private credit lending, but from asset backed finance or broadly syndicated loan (BSL) structures where complexity or opacity enabled alleged misconduct to go unnoticed.

These incidents typically involved inflated collateral values or misrepresented receivables within loan portfolios that had been securitised or sold into private credit vehicles. Their significance lies not in direct contagion, as they represented a small fraction of the roughly US$1.8 trillion global private credit market,11 but in the way they knocked investor confidence just as several large retail targeted private credit funds/BDCs were struggling to manage redemptions.

Fraud linked asset write downs amplified a sense of fragility already brewing in private credit structures that promised liquidity on illiquid loans. The result was heightened scrutiny of valuation practices, internal audit controls, and the independence of fund administrators, issues that the US Securities and Exchange Commission subsequently began formally investigating in early 2026.12

Key takeaways

These fraud incidents were isolated but revealed that complexity and illiquidity, rather than traditional mid market private lending, remain fault lines in private credit.

The episodes reinforce the importance of scrutinising fund structures, valuation governance, and independent oversight, particularly in retail oriented vehicles. Due diligence should place greater emphasis on transparency, and how managers handle a host of stresses, not just yields or historic default rates.

Return compression is not credit deterioration

Lower reported private credit returns have also been receiving attention. Much of the change in returns this year has been driven not by credit losses, but return compression, a mechanical consequence of falling base rates rather than any deterioration in loan quality.

Most US private credit loans are structured as floating rate instruments priced at

Secured Overnight Financing Rate (SOFR is the base interest rate most US floating rate private credit loans are priced off) + a fixed credit spread. For example:

- SOFR + 500 basis points

- SOFR + 600 basis points

The credit spread compensates lenders for credit, illiquidity, and structural risks and remains fixed for the life of the loan. The SOFR component, by contrast, is a floating base rate that resets daily or monthly in line with short term US interest rates.

As the US Federal Reserve began signalling policy easing in late 2025, SOFR declined from around 5.3% to 3.6-3.7% by late March 2026,13 reducing the coupon paid to investors even when credit fundamentals stayed constant. So, when headlines claim that “private credit returns are falling,” what they are describing is a normal income reset, not weakening portfolio performance.

Spreads in mid market direct lending portfolios remain in the 450 550 basis points range,14 consistent with historical averages, and while defaults are expected to rise from their 2-2.5% historical average,15 we think this would be a step towards normalisation, rather than something untoward.

In our view, default rates in private credit have been unusually low since the asset class came of age after the Global Financial Crisis, and any uptick would represent a long overdue reset that helps reallocate capital toward stronger borrowers, better underwriting standards, and more stringent valuations.

In short, lower coupon income reflects the declining SOFR base rate, not rising borrower risk. As we see it, underlying loans continue to perform, and credit spreads have held firm, reflecting continued lender discipline.

Key takeaways

Falling base rates, on the back of the US Federal Reserve signalling policy easing, are compressing income, and thus reduce total yield in floating rate portfolios. Nonetheless, credit spreads are consistent with historical averages and so private credit portfolio risk return trade offs are for practical purposes, largely unchanged.

We have not observed meaningful loan quality loan quality deterioration, but income resets are now adjusting to easier policy conditions. All up, the adjustment for the asset class relates to valuation and liquidity repricing, not credit distress.

Concentration risks in software challenged by artificial intelligence (AI) disruption

The software sector, long viewed as an engine of stable growth within private credit portfolios, has arguably become the asset class’s most closely watched point of exposure of late. There are estimates that software companies and adjacent sectors represent around 30% of investment cost and fair value in BDC portfolios.16

This was not a source of vulnerability when lenders viewed software companies as near bulletproof borrowers, businesses with recurring revenues and strong cash flows. However, the advent of AI driven disruption has upset that happy picture, exposing structural overweights in business models now facing margin pressure, contract churn, and pricing compression.

The concern intensified in early 2026 as software related public equities experienced significant drawdowns amid AI repricing. Private lenders that had extended generous covenant lite loans to subscription-based platforms are now contending with slowing renewals, higher customer acquisition costs, and aggressive revenue cannibalisation by generative AI alternatives.

BDCs and direct lending platforms with legacy software concentrations have been enduring valuation markdowns on software and business services exposures, particularly cloud-based workflow and marketing technology firms whose client retention rates have slipped below historical averages.17

Unlike public markets, such as equity market valuations which adjust instantly, private credit loans are marked quarterly at manager discretion, leaving valuation lags that can obscure risk until refinancing events force repricing.

Many mid market software borrowers that thrived in the low-interest rate era of 2019 2022 are now contending with higher interest burdens, and AI disruption. These pressures explain the credit spread widening evidence in tech exposed loans, even as overall portfolio quality remains sound.

Key takeaways

In our view, asset concentration, in software and adjacent sectors, is the issue, not credit quality more generally. AI disruption is forcing a repricing of private credit’s technology premium.

Well diversified portfolios, with strong covenants, like ours, are better placed to absorb disruptions like those hitting software. Stress lies with over exposed managers whose software weightings exceed what we regard as prudent diversification limits, or whose loan covenants were too thin to allow early intervention.

Diversification is a hallmark of our private credit investments, and this is underscored by the fact that our “Software and Services” exposure is around 11%.

Furthermore, we impose a maximum 20% limit on sector exposures, and a 15% maximum limit to subsectors of software.

All up, what is occurring is not systemic credit failure, in our view. Instead, it is an idiosyncratic correction concentrated in a sector that grew very swiftly and now faces a recalibration as AI reshapes competitive economics.

How we participate in private credit

Investment discipline, strong risk-control and governance are hallmarks of our private credit practice.

Across our private credit portfolio, average free cash flow coverage is around 2.0x, meaning borrowers are generating roughly twice the free cash flow needed to service their debt obligations.

As the program grows, we expect to lend to roughly 200 borrowers, limiting our exposure to no more than 2% of any borrower’s total borrowings. Strict investment discipline, evidenced by a broad range of individual borrowers, ensures that no single issuer represents a material concentration within the portfolio, and thus meaningfully reduces idiosyncratic risk while supporting the stability and resilience of returns.

Moreover, we only lend to borrowers generating free cashflows from day one of the loan and with records of reliable earnings. We do not and will not deploy our clients’ capital to ‘blue sky’ companies with promises of great future returns but threadbare financial capacity on day one.

Considering current stresses facing software companies, our disciplined focus remains on businesses, including software companies, with stable, recurring revenue models, while excluding early stage or pre revenue companies that have yet to demonstrate meaningful commercial traction.

The companies we are lending to currently generate an average EBITDA of approximately A$68 million, placing them firmly in the middle market segment. These borrowers continue to demonstrate a meaningful premium relative to broadly syndicated loans (BSLs).

The premiums reflect the compensation for illiquidity embedded in the private credit market and emphasises that our clients are being appropriately rewarded for providing capital in a less liquid but fundamentally robust segment of the market.

The average loan to valuation ratio across our private credit portfolio is under 40% which provides a substantial margin of safety should asset values decline. This conservative positioning ensures that the companies we lend to are not taking on excessive impairment risk. By contrast, we continue to see areas of the market with aggressive capital structures exhibiting levels of risk we would not contemplate under any circumstances.

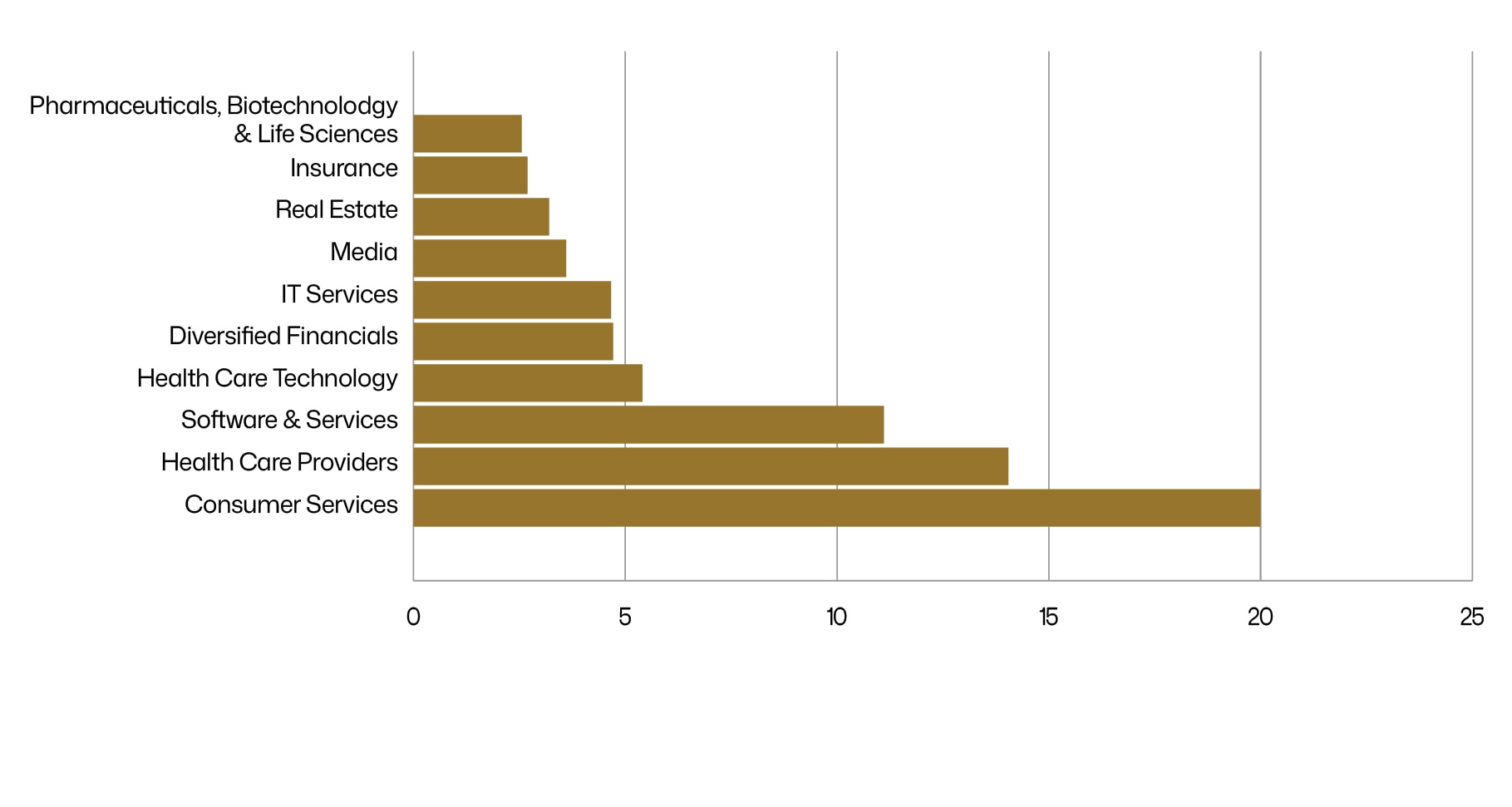

As noted earlier, we have modest exposure to software of around 11%, consistent with our emphasis on broad industry diversification and strict maximum industry and subsector allocations (Chart 1).

Chart 1: Well diversified industry allocations*

Anticipated industry allocations consistent with Strategic Asset Allocation (%)

*Top 10 industry allocations, totalling 71.94%, are shown

As at 31 December 2025

Source: MLC Asset Management

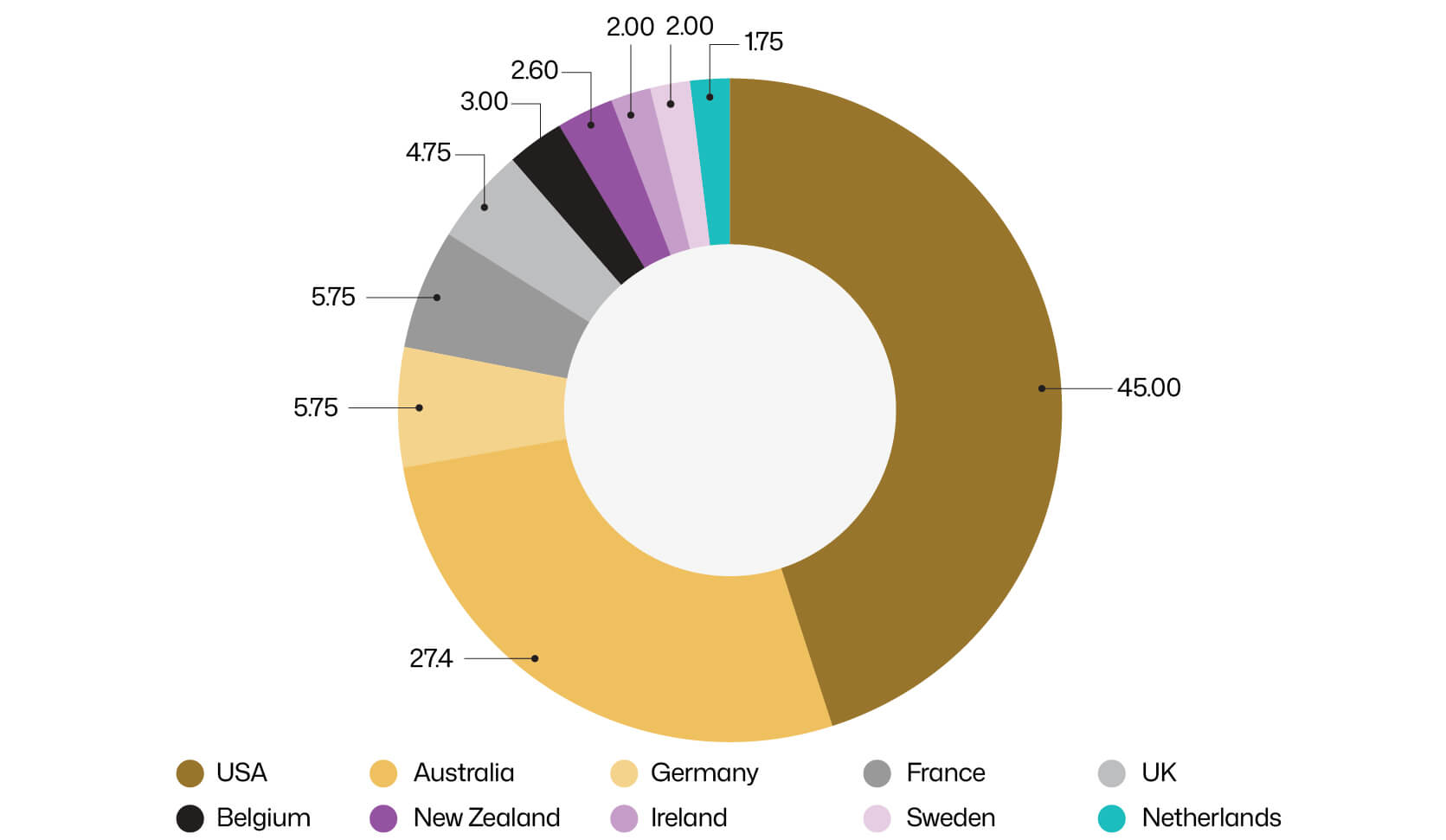

Meanwhile, our geographical exposure is dominated by allocations to the US, and Australia (Chart 2) both jurisdictions we are highly familiar with and in which we have very strong manager relationships.

Chart 2: Allocations in the US and Australia dominate our private credit investments

Geographical allocations consistent with Strategic Asset Allocation (%)

As at 31 December 2025

Source: MLC Asset Management

Stringent covenants provide strong lender protections

No investment is risk free, and private credit is no exception. That said, our program is deliberately built with structural and contractual guardrails designed to mitigate the risks inherent in direct lending.

Through bespoke investment mandates in our stand alone, fund of one arrangements with specialist private credit managers, we retain control over key underwriting standards. These mandates require stringent covenants and conservative loan terms, including low leverage and strong interest coverage ratios, giving us confidence in borrowers’ ability to service their debt across a range of conditions.

Importantly, we also maintain full transparency over the underlying loans originated by our appointed managers. This level of visibility is markedly different from the experience of investors accessing private credit through pooled retail vehicles, where insight into individual exposures is often limited.

A core element of our risk management approach is the use of robust financial and reporting covenants. These typically include leverage caps (such as debt to EBITDA limits), minimum interest coverage requirements, and contractual obligations for borrowers to provide early warning indicators of stress. Together, these covenants give lenders meaningful intervention rights well before a default scenario emerges.

We see this discipline as a key point of differentiation from covenant lite structures prevalent in broadly syndicated loans and high yield bonds. In our view, the ability to design and enforce tailored covenants has contributed to the stability of our private credit exposures, particularly when compared with the volatility experienced in some US retail focused vehicles.

This conservative positioning underpins our decision to avoid large cap, liquidity promised BDCs. It also reinforces our assessment that recent stresses in parts of the private credit market reflect vehicle design and investor behaviour rather than a broad deterioration in underlying credit quality.

Finally, our emphasis on higher quality loans with maturities, on average, of five years, has further supported the resilience of the program, helping to limit valuation and refinancing risks as market conditions evolve.

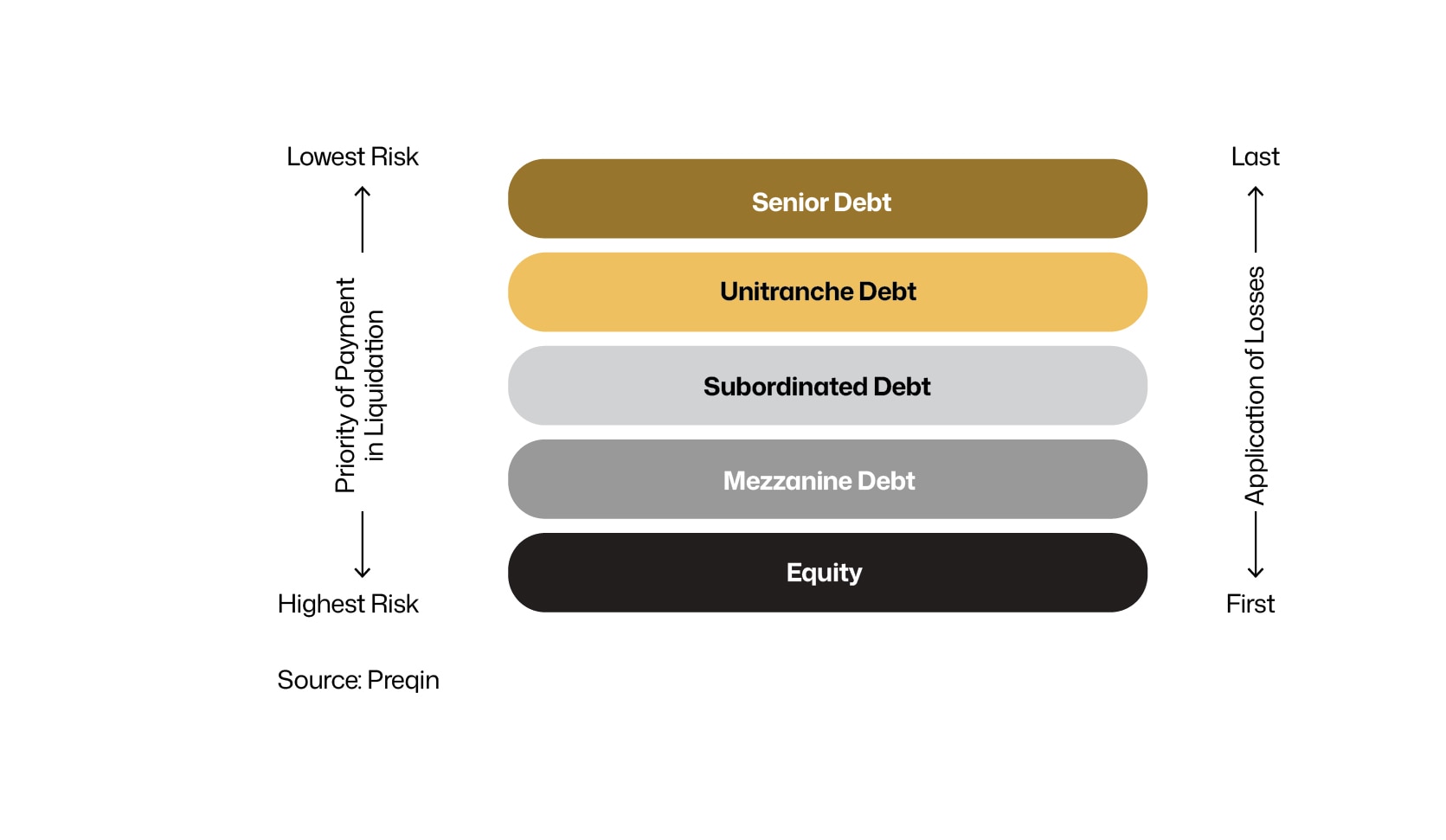

Loans high in the capital structure protect lenders

Our loans, fall into the senior secured category, and are high in the capital structure, which provides a level of safety in the event they become impaired. Senior secured lending typically offers stronger protection for investors compared with subordinated or mezzanine exposures, particularly when collateral values fluctuate.

Our focus on senior secured lending means that they have the strongest protection for investors within the capital structure (Chart 3) and this category of loan takes precedence for repayment in the event of borrower default. It holds a higher priority within the capital structure compared to more junior debt, as well as equity, and is the security in the capital structure which suffers losses last.

One of senior debt’s key features is that it is usually secured by collateral or assets, granting the lender a “first lien” claim over them. This security measure contributes to its lower risk profile when compared to junior debt or equity.

Due to its lower risk, lenders often offer senior debt at more favourable interest rates than those charged for junior or subordinated debt. This combination of priority and reduced risk makes the senior debt an attractive option for both borrowers and lenders seeking stability and security in their financial transactions.

Chart 3: As senior debt in the capital structure, private credit investors have priority of payment in the event of liquidation

Importance of manager due diligence

To be clear, covenants in and of themselves do not guarantee avoidance of losses. Manager selection, strong governance, and the due diligence that goes into the selection process provide us with a margin of comfort where we utilise private credit in our portfolios.

The private credit managers we partner with are specialists with long histories of managing credit through investment cycles and the deep resources to carry out remedial action, should stresses appear among borrowers.

Each of our private credit managers specialise in specific parts of the private credit realm by borrower size ranging from large companies to mid-size and even small companies.

All up, when practised to strict institutional standards, we think private credit can continue to be a source of attractive risk-adjusted returns.

1 https://bluevaultpartners.com/nontraded-bdc-fundraising-asset-levels-balloon-in-q3/

2 As above

3 markets.financialcontent.com/wedbush/article/marketminute-2026-2-20-the-private-credit-crack-up-blue-owls-14-billion-fire-sale-sends-shockwaves-through-wall-street

4 Franklin Credit Management Corporation - The "Blue Owl" Crack-up: Why Private Credit’s Golden Era Just Hit a Wall

5 Private Credit News Weekly Issue #91: The Redemption Wave Goes Systemic as Blue Owl Burns and Contagion Spreads

6 As above

7 Southern District of New York | First Brands Executives Charged With Multibillion-Dollar Fraud | United States Department of Justice

8 Southern District of New York | CEO, CFO, COO Charged In Connection With Billion-Dollar Collapse Of Tricolor Auto | United States Department of Justice

9 BlackRock and BNP Paribas Hit by $500 Million Private Credit Fraud - Fincrime Central

10 MFS’s Collapse Refuels Double-Pledging Concerns Within the Private Credit Industry - Manatt, Phelps & Phillips, LLP

11 More Cracks Emerge in Private Credit's $1.8 Trillion Iceberg - Americans for Financial Reform

12 Private Credit Under SEC Scrutiny as Liquidity Pressures Rise - ACA Group

13 https://fred.stlouisfed.org/series/SOFR

14 Private Credit Perspectives Q1 2026

15 Private credit’s ‘zero-loss fantasy’ is ending as rising defaults loom

16 https://octus.com/resources/articles/octus-private-credit-software-analysis-reveals-almost-30-exposure-to-bdcs/

17 Private Credit News Weekly Issue #91: The Redemption Wave Goes Systemic as Blue Owl Burns and Contagion Spreads

Important information

This communication is issued by MLC Investments Limited ABN 30 002 641 661 AFSL 230705, IOOF Investment Services Ltd ABN 80 007 350 405 AFSL 230703 and OnePath Funds Management Limited ABN 21 003 002 800 AFSL 238342 each in their capacity as responsible entity and trustee of the various funds issued by them. These entities are part of the Insignia Financial group of companies comprising Insignia Financial Ltd ABN 49 100 103 722 and its related bodies corporate (Insignia Financial Group).

The information in this communication is intended for wholesale clients (as defined under the Corporations Act 2001 (Cth) in Australia.

The information and commentary provided in this communication is of a general nature only and does not relate to any specific fund or product issued by an Insignia Financial Group entity. The information does not take into account any particular investor’s personal circumstances and reliance should not be placed by anyone on the information in this communication as the basis for making any investment decision. Before acting on the information, you should consider the appropriateness of it having regard to your personal objectives, financial situation and needs. You should consider the relevant Product Disclosure Statement (PDS) and Target Market Determination (TMD), available from the applicable Insignia Financial Group website or by calling us, before deciding to acquire or hold an interest in a financial product issued by an entity within the Insignia Financial Group.

Past performance is not a reliable indicator of future performance. The value of an investment may rise or fall with the changes in the market. Actual returns may vary from any target return described and there is a risk that the investment may achieve lower than expected returns. Any reference in this communication to a specific company is for illustrative purposes only and should not be taken as a recommendation to buy, sell or hold securities or any other investment in that company. Securities mentioned in this communication may no longer be in our funds after the time of preparation.

No company in the Insignia Financial Group guarantees the repayment of capital or the performance of an investment, unless expressly stated in a PDS. Any investment is subject to investment risk, including possibly delays in repayment and loss of income and principal invested.

Any opinions expressed constitute our judgement at the time of issue and are subject to change without notice. We believe that the information contained in this communication is correct and that any estimates, opinions, conclusions or recommendations are reasonably held or made at the time of compilation. However, no warranty is made as to their accuracy or reliability or in respect of other information contained in this communication. Any projection or forward-looking statement (Projection) in this communication is provided for information purposes only. No representation is made as to the accuracy or reasonableness of any such Projection or that it will be met. Actual events may vary materially.

This communication is directed to and prepared for Australian residents only.